-

Suggested IWM/GDX Allocation Levels

A discussion in this thread triggered the idea to update this thread weekly with "modeled" or "idealistic" minimum risk allocations for the IWM and GDX robot.

Suggested IWM/GDX allocations for minimum portfolio volatility:

IWM: 73%

GDX: 27%

This is a walk-forward test to determine the variability of this allocation. Use at your own peril...

The next update will be the weekend of June 25th.

===================

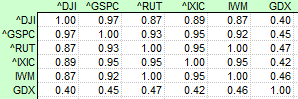

Correlation Matrix:

Posting Permissions

Posting Permissions

- You may not post new threads

- You may not post replies

- You may not post attachments

- You may not edit your posts

Forum Rules

Reply With Quote

Reply With Quote